PTJ

Last week legendary money manager Paul Tudor Jones made a case for owning bitcoin as a hedge against monetary deflation.

“I am not an advocate of Bitcoin ownership in isolation, but do recognize its potential in a period when we have the most unorthodox economic policies in modern history. So, we need to adapt our investment strategy. We have updated the Tudor BVI offering memoranda to disclose that we may trade Bitcoin futures for Tudor BVI. We have set the initial maximum exposure guideline for purchasing Bitcoin futures to a low single digit exposure percentage of Tudor BVI’s net assets, which seems prudent. We will review this exposure guideline regularly.”

“But the GMI caused me to revisit Bitcoin as an investable asset for the first time in two and a half years. It falls into the category of a store of value and it has the added bonus of being semi- transactional in nature. The average Bitcoin transaction takes around 60 minutes to complete which makes it “near money.” It must compete with other stores of value such as financial assets, gold and fiat currency, and less liquid ones such as art, precious stones and land. The question facing every investor is, “What will be the winner in ten years’ time?”

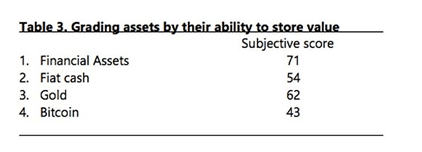

His firm ranked bitcoin against cash, gold, and financial assets based on 4 characteristics:

- Purchasing Power – How does this asset retain its value over time?

- Trustworthiness – How is it perceived through time as a store of value?

- Liquidity – How quickly can it be monetized into a transactional currency?

- Portability – How easy is it to move based on unforeseen circumstances?

“Bitcoin had an overall score nearly 60% that of financial assets but has a market cap that is 1/1200th. It scores 66% of gold as a store of value, but has a market cap that is 1/60th of gold’s outstanding value.“